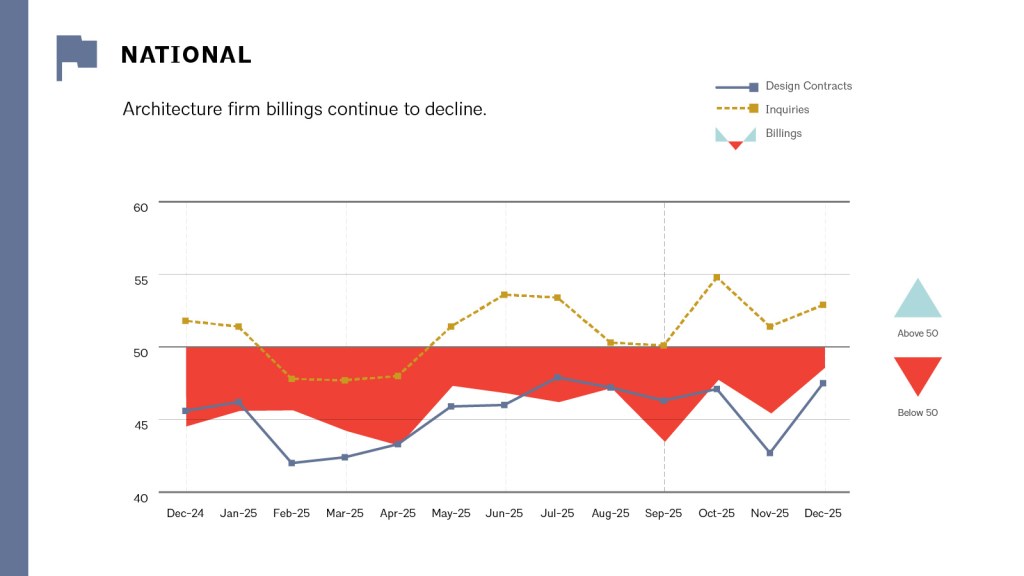

The long-anticipated turnaround in architecture’s business cycle never materialized in 2025. Instead, the year closed with the profession still firmly in contraction—less severe than earlier months, perhaps, but no closer to a true recovery.

The AIA/Deltek Architecture Billings Index (ABI) finished December at 48.5, up from 45.3 in November. While the uptick suggests that fewer firms reported declining billings at the end of the year, the index remained below the critical threshold of 50 that separates growth from contraction. In practical terms, the modest improvement signals stabilization rather than reversal—and offers little evidence that a rebound is imminent.

That conclusion is reinforced by the broader trajectory of the past three years. Architecture firm billings declined throughout 2025 and in most months since October 2022, with only three brief interruptions. Even as December’s data shows some easing in the pace of decline, other leading indicators point in the opposite direction. The value of newly signed design contracts continues to fall, suggesting that any near-term recovery in firm revenues remains unlikely.

And yet, the industry’s underlying workload tells a more complicated story.

Despite weakening billings, firm backlogs remain historically strong, averaging 6.3 months across the profession. Large firms—those with annual billings of $5 million or more—report an average backlog of 8.6 months, while institutional practices average 8.2 months. In other words, many firms are still busy, even as the pipeline that feeds future work shows signs of erosion.

That contradiction—strong backlogs paired with weakening demand—has defined architecture’s post-pandemic economy. Project inquiries have declined from earlier highs, and the value of newly signed contracts continues to soften. But for now, the accumulated work of previous years has prevented a sharper collapse, allowing firms to maintain staffing levels and workloads longer than expected.

According to AIA Chief Economist Kermit Baker, Hon. AIA, PhD, the December data offers a handful of tentative bright spots—though not enough to alter the broader outlook.

“Despite the ongoing decline in billings at most architecture firms, there are a few signs of potential improvement on the horizon. The number of inquiries into future project work continues to grow, and Midwest firms saw billings increase for the fourth consecutive month in December,” said Baker. “In general, however, overall conditions remain weak across all specializations. Multifamily residential firms faced the steepest declines, while institutional firms experienced a slightly slower pace of decline compared to earlier in the year.”

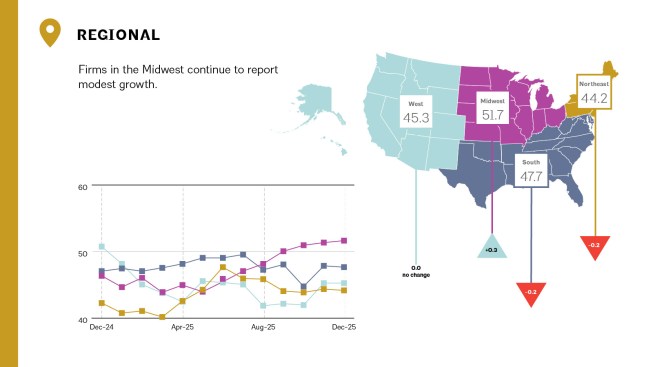

Regionally, the Midwest continues to outperform the rest of the country, posting a December regional average of 51.7—its fourth consecutive month above 50. The South followed at 47.7, while the West registered 45.3 and the Northeast lagged at 44.2. These figures, calculated as three-month moving averages, underscore the uneven geography of the downturn: resilience in some markets, deep contraction in others.

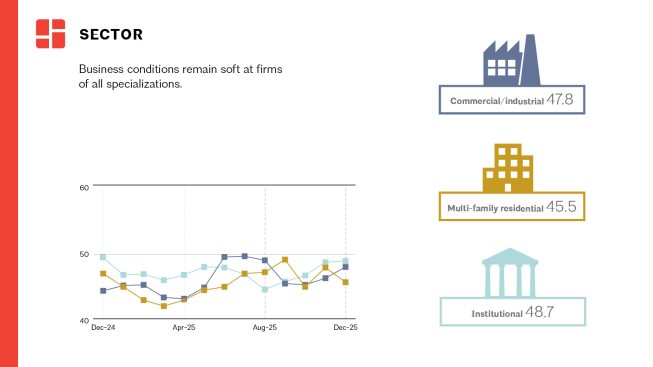

The sector breakdown tells a similarly uneven story. Institutional firms posted the strongest performance in December, with a sector index of 48.7, followed by commercial and industrial practices at 47.8. Multifamily residential firms continued to struggle, registering 45.5, while mixed-practice firms reported the weakest conditions overall at 44.0.

Leading indicators provide little reassurance that the industry is on the cusp of recovery. The project inquiries index came in at 52.9—still in positive territory, but well below the levels seen earlier in the cycle. More troubling is the design contracts index, which remained in contraction at 47.5, signaling continued softness in the commitments that translate into future billings.

Taken together, the December ABI paints a picture of an industry suspended in an uncomfortable holding pattern. Firms remain busy, supported by backlogs built during strongerader years. But new work is arriving more slowly, contracts are shrinking in value, and the long-promised rebound keeps receding into the future.

As architecture enters 2026, the question is no longer when growth will return—but how long firms can continue to navigate an economy defined by persistent uncertainty, delayed decisions, and a recovery that never quite arrives.