After months of steady decline, the architecture industry may be approaching a turning point—or at least a pause in its downward trajectory.

The latest AIA/Deltek Architecture Billings Index (ABI) for February registered a score of 49.4, a notable increase from January’s 43.8. While still below the critical threshold of 50—indicating that more firms are reporting declining billings than increasing ones—the upward movement suggests that the pace of contraction is slowing.

That distinction matters. For an industry that often functions as a leading indicator of broader construction activity and economic health, even a modest shift can signal deeper structural changes ahead.

Yet if February’s data offers a glimmer of stabilization, it also reveals an industry caught in a precarious holding pattern—one shaped as much by macroeconomic uncertainty as by internal resilience.

A Rebound in Interest, but Not in Commitment

One of the clearest signs of cautious optimism lies in the rebound of project inquiries, which rose to 52.3 after dipping in January. The increase suggests that clients are once again exploring potential projects, re-engaging with architects after a period of hesitation.

But that renewed interest has not yet translated into firm commitments.

Newly signed design contracts continued to decline in February, albeit at a slower rate than in previous months. This divergence—rising inquiries paired with falling contracts—points to a familiar dynamic in uncertain economic cycles: clients are asking questions, but they are not yet ready to act.

In practical terms, firms may be seeing more activity in early-stage conversations while still facing a constrained pipeline of secured work.

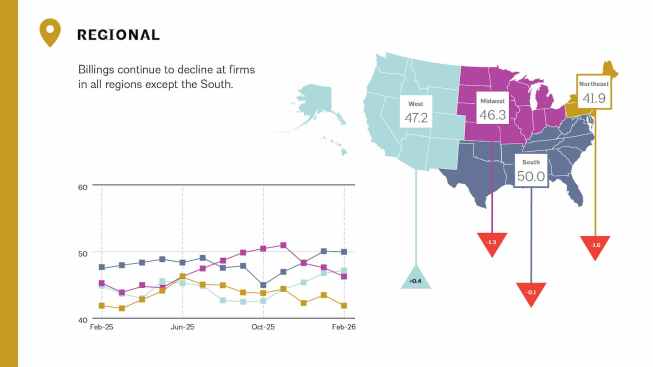

A Regionally Uneven Slowdown

Geography continues to shape the contours of the downturn.

The South emerged as the only region to reach equilibrium, posting a score of 50.0 for the second consecutive month. Elsewhere, conditions remain weaker. The West (47.2) and Midwest (46.3) continued to contract, while the Northeast lagged significantly at 41.9—its performance likely exacerbated by winter storms that disrupted both construction activity and project timelines.

This regional divergence underscores how localized factors—from weather to economic policy—are compounding broader national trends.

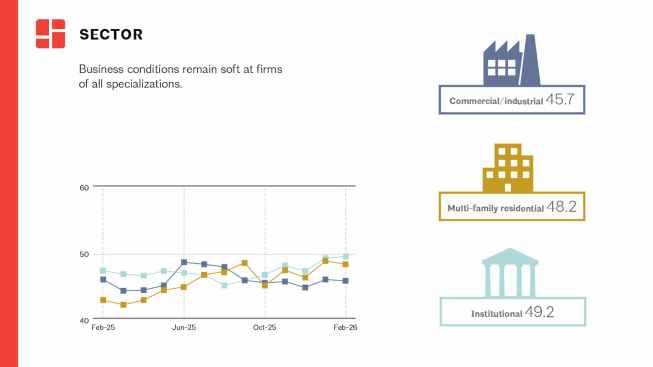

Sectoral Fragility, with One Exception

Across sectors, the story is largely one of continued softness.

Commercial and industrial work remains particularly weak, with a score of 45.7, reflecting ongoing uncertainty in corporate investment and development. Mixed-practice firms—often more exposed to volatile project types—reported the lowest performance at 41.8.

Multifamily residential, long a driver of architectural billings, registered 48.2, suggesting that even this once-resilient sector is losing momentum.

Institutional work, however, appears to be holding steadier than the rest. With a score of 49.2, it is the closest to stabilization among all sectors, buoyed perhaps by public funding streams and longer project timelines that insulate it from short-term market shocks.

Firms Expect Stability—But Not Growth

In a new quarterly question introduced by the AIA, firm leaders were asked to forecast how their billings would change in the coming quarter.

The responses reveal a profession bracing for stagnation rather than recovery.

Nearly half (48 percent) of respondents expect billings to remain unchanged in the second quarter of 2026. Another 31 percent anticipate modest growth of 5 percent or more, while 21 percent foresee a comparable decline.

The distribution suggests a fragmented outlook, with no clear consensus on where the market is heading—only a shared recognition that volatility remains the defining condition.

A Broader Economy Still Under Strain

Any reading of the ABI must ultimately be situated within the larger economic context, which remains unsettled.

“While the ABI data shows some positive trends, the broader economy continues to struggle, with unemployment increasing in February,” said AIA Chief Economist Richard Branch. “However, architectural services employment remained steady in January at 204,600, up nearly 2,000 positions from a year ago.”

Branch’s assessment captures the central tension of the current moment: signs of resilience within the profession are unfolding against a backdrop of broader economic fragility.

The stability in architectural employment, in particular, suggests that firms are not yet responding to reduced billings with widespread layoffs—an indication that many may be anticipating a near-term rebound or are choosing to hold onto talent in a tight labor market.

Stabilization—or a Temporary Plateau?

Taken together, February’s data paints a picture of an industry that is no longer in free fall—but is far from recovery.

The slowing rate of decline, rising inquiries, and steady employment all point toward stabilization. But the continued weakness in contracts, uneven regional performance, and uncertain economic outlook suggest that this stabilization may be more of a pause than a turning point.

For architects, the implications are clear: the pipeline is active, but fragile; opportunities exist, but require patience; and the next phase of the cycle remains deeply contingent on forces beyond the discipline itself.

In other words, the profession is not yet climbing out of the downturn—it is learning how to operate within it.